The Fragile Decade: Why the First Years of Retirement Can Make or Break Your Future

Most people believe retirement success depends mainly on how much money they save.

In reality, timing can matter just as much as savings.

Financial planners call the period about five years before and five years after retirement the Fragile Decade. This is a window when your financial future is unusually vulnerable to market swings, big decisions, and unexpected events.

During this time, your savings are usually at their highest; you stop contributing and start withdrawing; there is little time to recover from losses; health risks begin to rise; and major lifestyle decisions often happen simultaneously. A single bad sequence of events can have lifelong consequences.

During the Fragile Decade:

A single bad sequence of events can have lifelong consequences.

Why Financial Literacy Matters

Understanding the Fragile Decade isn’t just for financial advisors; it’s a key part of financial literacy.

Knowing how markets, withdrawals, inflation, and life events interact allows you to make informed decisions rather than reactive ones. The more you understand your money, the better you can plan, protect your lifestyle, and avoid costly mistakes. In short, financial literacy turns knowledge into security, giving you control over your retirement instead of letting circumstances dictate it.

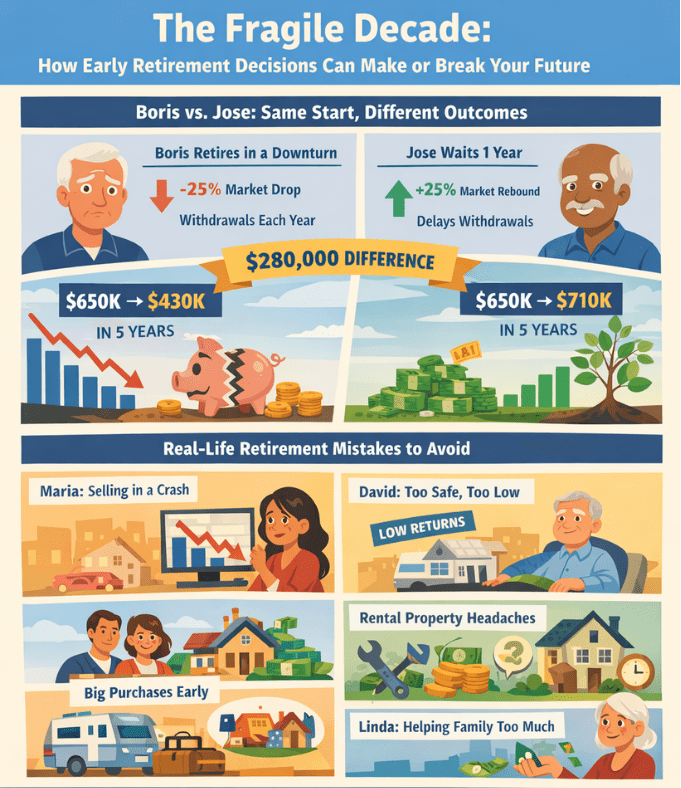

Boris and Jose: Same Savings, Very Different Outcomes

Boris and Jose both retire at age 65 with nearly identical portfolios:

$650,000 each

Planned withdrawals: $40,000 per year

Expected long-term return: about 6% annually

The only difference is timing.

Boris Retires Into a Downturn

Boris retires immediately, just before a major market decline.

Assumptions:

- Year 1: −25% market drop

- Years 2–5: +6% annual return

- Withdrawals continue every year

Because he needs income, Boris must sell investments when prices are low, locking in losses.

After five years, his portfolio is approximately $430,000

Even though markets recover, his savings never fully catch up.

Lesson: Early withdrawals during downturns can permanently shrink your nest egg.

Jose Waits One Year

Jose decides to work one more year and delay withdrawals.

Assumptions:

- Year 1: +25% recovery year

- Years 2–5: +6% annual return

- Withdrawals begin after the first year

Jose avoids selling during the downturn and benefits from the recovery.

After five years, his portfolio is approximately $710,000

Lesson: Waiting even one year before withdrawing can dramatically improve long-term outcomes.

One Decision, $280,000 Difference

After only five years, Boris has about $430,000 while Jose has about $710,000, creating a gap of roughly $280,000. Both started from the same point, yet timing alone caused a dramatic difference that could continue to widen over a 20–30-year retirement. As a result, even small timing decisions can have lasting effects.

Why This Happens: Sequence-of-Returns Risk

Investment averages don’t tell the whole story. What matters is the order of returns. Early losses combined with withdrawals permanently reduce your capital, limit future growth, and increase the risk of running out of money.

This is the central danger of the Fragile Decade.

Real-Life Mistakes That Amplify the Risk

Besides market timing, other common mistakes can make the Fragile Decade even riskier. Let’s look at real-life examples.

Maria. Forced to Withdraw During a Crash

Maria retires just before a severe downturn.

Her portfolio falls sharply, but her living expenses remain unchanged. She withdraws money while prices are low, permanently shrinking her investment base.

Even after recovery, her savings never return to their original trajectory.

Lesson: Early withdrawals during losses cause lasting damage.

David. Playing It Too Safe

David moves all his retirement savings into very low-risk accounts to avoid volatility.

His income becomes stable, but inflation steadily erodes purchasing power. Over time, his “safe” portfolio fails to keep up with rising costs.

By his late 70s, he faces a declining lifestyle and shrinking reserves.

Lesson: Avoiding risk entirely can create a different kind of danger.

Tom and Nancy. Large Purchases Too Soon

Excited about retirement, the couple uses substantial savings to:

- Buy a vacation property

- Upgrade their home

- Help adult children financially

- Travel extensively

Their nest egg shrinks dramatically before it has time to support decades of withdrawals.

Lesson: Big early spending reduces long-term resilience.

Linda. Supporting Family at Her Own Expense

Linda frequently helps her adult children and grandchildren with expenses.

Individually, each contribution seems manageable. Over time, however, these transfers significantly reduce her financial cushion.

When unexpected medical bills arise, she has little margin left.

Lesson: Generosity can unintentionally compromise long-term security.

Why the Fragile Decade Is So Dangerous

During the Fragile Decade, retirees often faced multiple risks simultaneously. Market volatility, rising healthcare costs, inflation, family obligations, and the possibility of living longer than expected can all put pressure on finances. Emotional decision-making after leaving work can make these challenges even harder to navigate. Once withdrawals begin, mistakes become more difficult to correct, making careful planning essential.

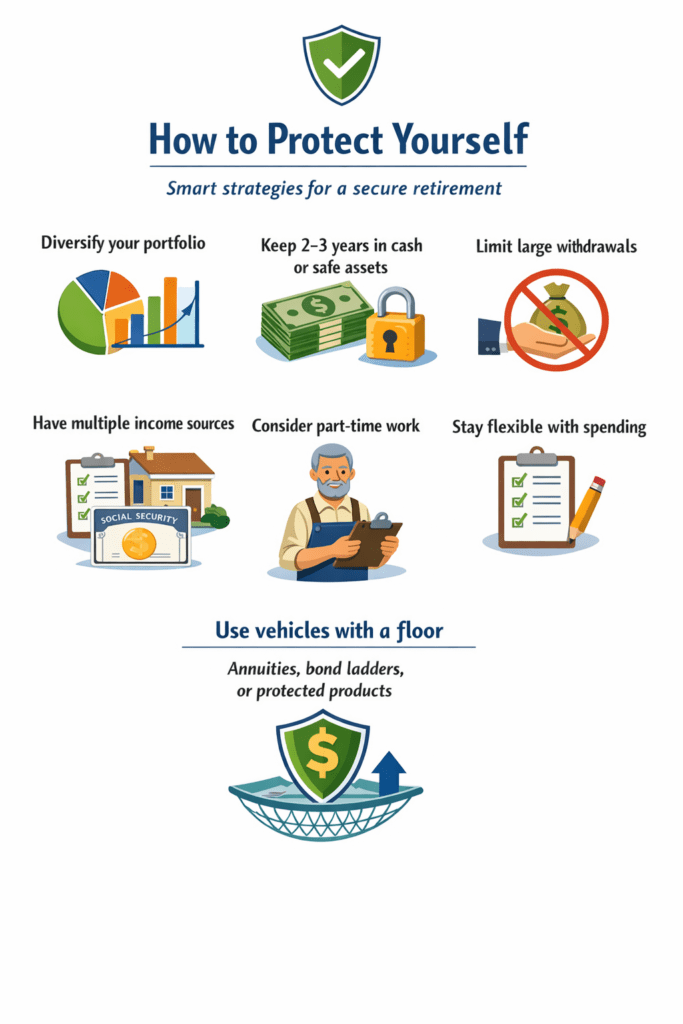

How to Protect Yourself

While no strategy eliminates risk, preparation can dramatically improve outcomes. Financial experts often recommend maintaining a diversified portfolio, keeping several years of expenses in safer assets or cash (typically 2–3 years), avoiding large withdrawals early in retirement, planning multiple income sources, staying flexible about spending, considering part-time work during downturns, reviewing plans regularly, and using vehicles with a floor, such as annuities, IUL insurances or structured products that guarantee a minimum balance to protect against severe market drops.

It’s also critical to account for taxes on Social Security benefits and Medicare premiums when planning withdrawals. These mandatory costs can reduce disposable income and affect the sustainability of your portfolio. Incorporating them into your budget early helps prevent surprises and ensures your retirement income lasts.

Finally, retirees should schedule complementary check-ins with financial, tax, and healthcare advisors. For example, annual or semi-annual meetings can help review investment allocation, tax strategies, and healthcare planning, keeping your plan aligned with market conditions and personal needs.

Sometimes, delaying retirement even briefly can have an outsized positive impact.

Planning for Outliving Your Money

In addition to managing the Fragile Decade, retirees should plan to avoid outliving their money, ensuring funds last throughout the remainder of their lives. Poor decisions early in retirement, like withdrawing too much during a downturn or spending heavily in the first few years, can jeopardize long-term financial security. Planning to outlive your money ensures you don’t run out of savings and can maintain your lifestyle for decades into retirement. Vehicles like annuities, diversified portfolios, and cash reserves can help protect both your early years and your long-term financial health.

The latest report from the National Council on Aging (NCOA) and LeadingAge LTSS Center at UMass Boston reveals a stark reality: older adults with the fewest financial resources die, on average, nine years earlier than those with the greatest wealth. This demonstrates that careful retirement planning isn’t just about comfort; it can directly impact longevity and overall quality of life.

The Fragile Decade: Key Takeaways for a Secure Retirement

Retirement success isn’t determined only by how much you save, but by how well you navigate the Fragile Decade. Boris and Jose started in the same place. One year of timing created a gap that may never close. Understanding this critical period and avoiding common mistakes can make the difference between lasting security and financial stress for the rest of your life.