Social Security in the United States: What Immigrants Should Know

For many people moving to the United States, understanding how the retirement system works can be confusing. The Social Security program is one of the most important parts of retirement planning in the U.S., but it is often misunderstood.

Social Security provides retirement income, disability benefits, and support for families of deceased workers. The program is funded through payroll taxes paid by employees and employers during a person’s working years.

However, Social Security was designed as basic financial support in retirement, not necessarily as the only source of income.

Who Can Receive Social Security Benefits?

Eligibility for Social Security benefits depends not only on your work history, but also on your legal status in the United States.

Generally, the following individuals may qualify for Social Security benefits if they have earned enough work credits:

U.S. Citizens

U.S. citizens who have worked and paid Social Security taxes for the required number of years (usually 40 credits) are eligible for retirement benefits.

Who Else Can Receive Social Security Benefits?

Lawful Permanent Residents (Green Card Holders)

Permanent residents can qualify for Social Security benefits if they have legally worked in the United States and paid Social Security taxes long enough to earn the required credits.

Certain Legal Non-Citizens

Some non-citizens with authorized work status may also qualify if they have a valid Social Security number, work authorization, and have paid Social Security taxes.

These may include individuals who worked in the U.S. under specific visas that allowed employment.

How Many Years Do You Need to Work

Eligibility for Social Security is based primarily on work history and contributions to the system, but legal status and authorization to work are also important factors.

40 work credits

to qualify for Social Security

To qualify for Social Security retirement benefits, you must earn 40 work credits, which usually equals about 10 years of work in the United States.

Workers can earn up to 4 credits per year, depending on their income and whether they pay Social Security taxes.

However, having 40 credits only makes you eligible for benefits. The amount you receive depends on your earnings history.

35 highest earning years

is counted

Social Security calculates benefits using your 35 highest earning years. If you worked fewer than 35 years in the U.S., the missing years are counted as zero income, which reduces the average and lowers your future benefit.

This is especially important for immigrants who arrive in the United States later in life.

Totalization Agreements with Other Countries

The United States has Totalization Agreements with several countries. These agreements help people who have worked in multiple countries combine their work credits to qualify for benefits.

However, the United States currently has Totalization Agreements with only 25 countries, meaning work history from those countries usually cannot be combined with U.S. Social Security credits.

Self-Employed Workers

Self-employed individuals also contribute to Social Security, but they pay taxes differently. Instead of sharing payroll taxes with an employer, self-employed workers pay the full self-employment tax (15.3%), which includes:

- Social Security tax

- Medicare tax

These contributions help build their future retirement benefits just like traditional employment.

Planning for a More Secure Retirement

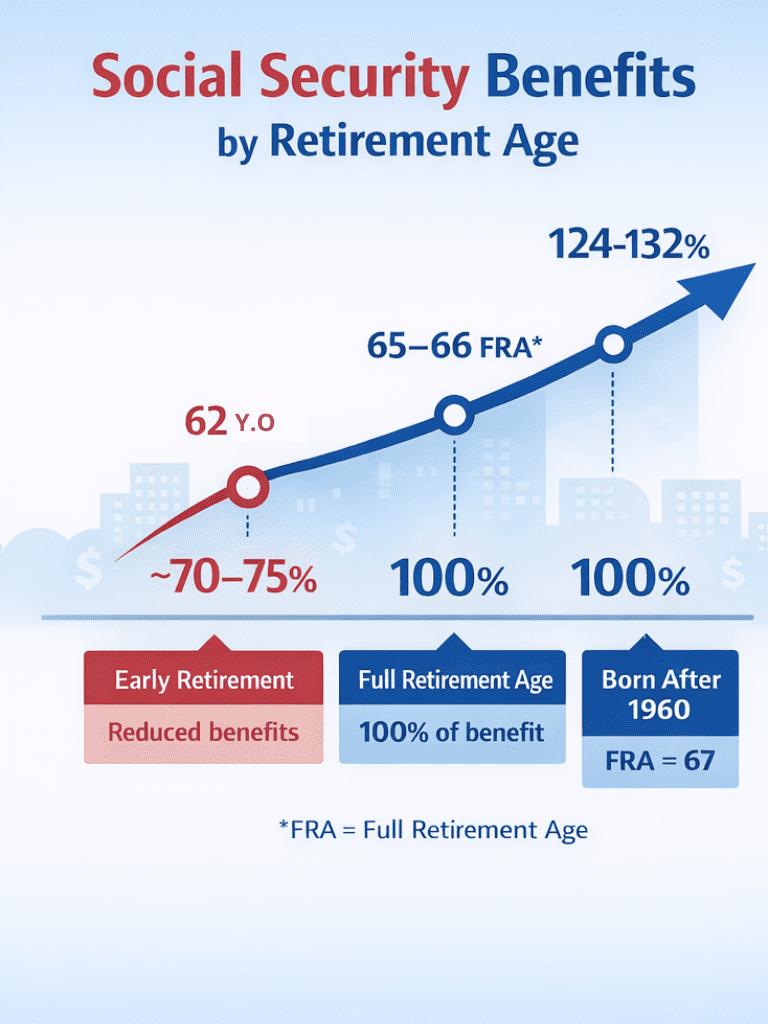

When To Claim Social Security?

62 vs 67 vs 70

If your full benefit at age 67 is $2,000 per month:

| Age | Monthly Benefit |

| 62 | ~70–75% of full benefit, ~$1,400 |

| 67 | 100%, $2,000 |

| 70 | ~124–132%, ~$2,480 |

Waiting longer can significantly increase your lifetime retirement income.

Social Security can be a valuable part of retirement income, but it is usually only one piece of the financial picture. Because of taxation, planning how you structure retirement income can help reduce taxes and preserve more of your savings.

A strong retirement plan often includes:

- personal savings

- investment accounts

- retirement plans such as 401(k), 403(b), or Traditional and Roth IRA

- life insurance with cash value as a flexible, tax-advantaged component

- long-term financial planning

Understanding how Social Security works helps immigrants make better financial decisions and build a more secure future in the United States.

It’s also important to be especially careful and conservative during the “fragile decade”, the 5 years before and after retirement, when financial decisions can have a lasting impact on your long-term security.

Social Security Benefits for Spouses

Many people don’t realize that a spouse who has little or no work history may still qualify for benefits. A spouse may receive up to 50% of the working spouse’s Social Security benefit once the working spouse files for retirement. This can be especially important for families where one spouse stayed home to care for children or worked fewer years.

Survivor Benefits: Financial Protection for Families

One of the most valuable but often overlooked parts of Social Security is survivor benefits. If a worker passes away, certain family members may qualify to receive monthly payments based on the worker’s earnings record.

Possible beneficiaries include:

• A surviving spouse

• Children under 18

• Disabled children

• Sometimes dependent parents

These benefits can provide critical financial support during difficult times. For example:

• A surviving spouse may receive up to 100% of the worker’s benefit depending on age.

• A surviving spouse caring for a child under 16 may receive benefits earlier.

• Children can receive benefits until age 18 (or 19 if still in high school).

Understanding these rules helps families prepare financially and avoid surprises.

Financial Literacy Matters

Understanding how the U.S. financial system works is one of the most valuable skills immigrants can develop. Many families never learn these concepts until it’s too late.

But with the right education and planning, Social Security can become a powerful piece of a long-term financial strategy. Financial literacy isn’t just about numbers.

It’s about helping families make confident decisions for their future.

Retirement Age in the United States

You can start receiving Social Security retirement benefits at age 62, but your payments will be permanently reduced.

The Full Retirement Age (FRA) depends on your birth year and is currently between 66 and 67 for most people.

If you delay claiming benefits until age 70, your monthly payments can increase because of delayed retirement credits.

Can You Work While Receiving Social Security?

Yes, it is possible to work and receive Social Security benefits at the same time, but there are some rules.

If you start receiving benefits before your Full Retirement Age and continue working, your benefits may be temporarily reduced if your earnings exceed a certain limit.

Once you reach Full Retirement Age, you can work and earn any amount without reducing your Social Security payments.

Taxes on Social Security Benefits

Many people are surprised to learn that Social Security benefits may be taxable depending on their total income.

The taxable portion is based on your combined income, which includes:

- part of your Social Security benefits

- wages or self-employment income

- investment income and other sources

Up to 50% to 85% of Social Security benefits may be subject to federal income tax, depending on your total income level.

Why Some Retirees Continue Working

For many retirees, Social Security provides important support but does not replace their full working income.

Research shows that many Americans continue working after retirement, often because:

- Personal savings are insufficient

- Living expenses increase with age

- healthcare costs grow over time

For immigrants who started working in the U.S. later in life, this can be especially relevant because they may have fewer working years contributing to Social Security.