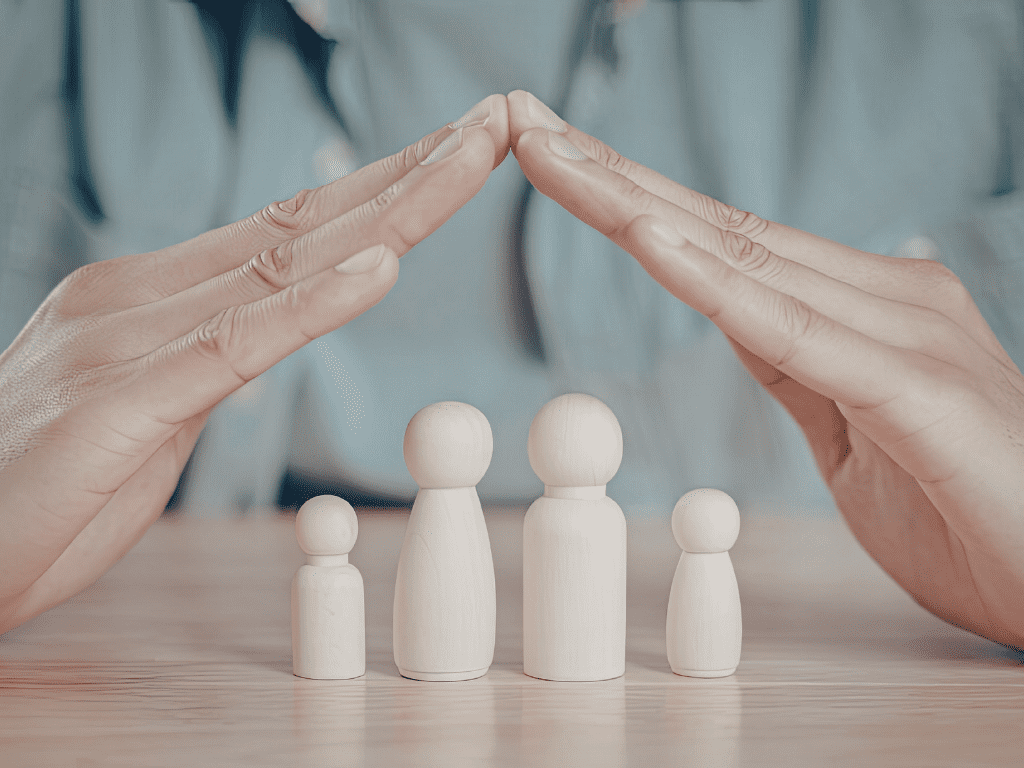

Insurance for Immigrants in the U.S.: Proper Protection.

The Second Milestone of Financial Literacy

Moving to a new country is exciting but also comes with responsibility, especially when it comes to protecting your family and finances. One of the most important steps immigrants can take is to get insurance.

In financial literacy frameworks like the 7 Money Milestones®, Proper Protection is the second milestone. Before building wealth, people need to ensure that a single accident, illness, or unexpected death won’t wipe out their hard work.

This guide explains the essential types of insurance immigrants should understand, including term life, whole life, Universal Life (UL), Variable Universal Life (VUL), disability, long-term care (LTC), hybrid policies, accelerated benefit riders, and other tools for financial security.

Why Insurance Matters

Insurance is important for everyone, regardless of age, income, or background, because life is unpredictable. For immigrants, the stakes can be even higher: families may rely on a single primary earner, support networks may be far away, and navigating a new country’s healthcare and financial system can be challenging. Proper insurance protects against these unique risks, ensuring that unexpected events don’t jeopardize their family’s stability or financial future.

Immigrant families often face unique risks:

- Limited local family support

- Financial obligations abroad

- Single primary earners

- Language and system barriers

- Lower or no eligibility for government benefits

Insurance creates a financial safety net that protects the family and personal future.

Who Is Eligible for Insurance in the U.S.?

Eligibility for life, disability, or long-term care insurance depends on immigration and tax status. Generally:

- Social Security Number (SSN) holders: Most policies require an SSN.

- ITIN holders: Some insurers accept an Individual Taxpayer Identification Number (ITIN), but coverage options may be limited.

- Certain visa holders: Temporary or long-term visas (like H-1B, L-1, or green card holders) are usually eligible, depending on the insurer’s rules.

Tip: Each company has its own rules. An experienced agent can help identify which policies you qualify for and find the best options for your situation.

Life Insurance: The Foundation of Family Protection

Life insurance replaces income if a breadwinner passes away, ensuring your family can maintain their lifestyle and cover essential costs.

Term Life Insurance (Temporary Coverage)

Term life insurance provides coverage for a set period (10, 20, or 30 years). Best for:

- Young families

- Mortgage protection

- Income replacement while children are dependent

- Budget-conscious households

Pros

- Affordable premiums

- High coverage amounts

- Simple to understand

- Can include LTC and disability protection (additional cost)

Cons

- Coverage expires at the end of the term

- No cash value

Best example: A 35-year-old parent buys a 20-year term policy to protect the family until the mortgage is paid and children are independent.

Permanent Life Insurance (Permanent Coverage + Cash Value)

Permanent life insurance lasts your entire life, provided premiums are paid. It also accumulates cash value, which you can access during your lifetime. Permanent life insurance lasts your entire life, provided premiums are paid. It also accumulates cash value, which you can access during your lifetime.

Many permanent insurance policies also include long-term care and disability riders by default, providing extra protection without the need to buy separate policies. They may cover long-term care, disability that prevents you from paying premiums or earning income, or even the treatment in case of a serious life-threatening illness.

Permanent life insurance combines protection with a savings component, a key tool for long-term financial security. There are a few types of permanent life insurance (whole life, UIL, VUL), and many options for designing a policy that meets the particular needs of an individual or family.

Best for

- Long-term financial planning

- Estate protection

- Leaving a guaranteed inheritance

- Business owners or permanent dependents

Pros

- Lifetime coverage

- Builds cash value

- Can include LTC and disability protection by default

- Can be used as a financial asset

- UIL has a floor – the protection against fluctuations and loss

Cons

- Higher premiums than term insurance

- Slower cash value growth in early years (for whole life)

Disability Insurance: Protect Your Income

The ability to work is the most valuable asset. Disability insurance replaces a portion of lost income if illness or injury prevents the insured from working. Why it matters: Without income, families struggle to pay rent, utilities, healthcare, and education. Long-term disability is statistically more likely than premature death during working years.

Note: Many permanent life insurance policies already provide disability coverage through included riders, helping protect income without the need for separate policies.

Types of Disability Policies

Short-Term Disability: Covers weeks to months; often employer-provided

Long-Term Disability: Covers years or until retirement; essential for sole earners and self-employed

Possible Features:

- Income replacement percentage (50–70%)

- Waiting period before benefits start

- Duration of benefits

- Definition of disability (own occupation vs any occupation)

Long-Term Care (LTC) Insurance

LTC protects against costs associated with nursing homes, assisted living, home care, or memory care. Options include:

Life Settlements with LTC Provisions – Sell existing policies for care funding (niche solution).

Standalone LTC Insurance – Dedicated policy covering home care or facility care.

Hybrid Life Insurance / Life + LTC Policies – Part of the death benefit can pay LTC expenses; unused benefits go to heirs.

Annuities with LTC Riders – Retirement income plus LTC benefits.

Accelerated Benefit Riders

Many life insurance policies include accelerated benefit riders, allowing early access to part of the death benefit if diagnosed with:

- Terminal illness

- Chronic illness

- Critical illness

Funds can cover medical care, home modifications, or daily living expenses.

Other Helpful Policy Riders

Waiver of Premium: Premiums paid if the insured becomes disabled

Child Rider: Coverage for children

Guaranteed Insurability: Increase coverage later without medical exams

How Much Coverage Do I Need?

Coverage = 10–15× annual income + debts + future obligations

Include:

- Funeral expenses

- Education costs

- Support for relatives abroad

- Replacement of unpaid household work

Important: There is no universal solution. Each family’s situation is unique. Free personalized guidance ensures your coverage fits your needs.

Building a Complete Protection Strategy

- Health Insurance

- Disability Insurance

- Term Life Insurance

- Whole Life / Permanent / UL / VUL (with LTC & Disability Riders)

- Long-Term Care Planning

Proper Protection: The Second Milestone of Financial Literacy

Insurance is about stability and control. Proper protection ensures:

✔ Family security

✔ Preservation of savings

✔ Peace of mind for wealth building

Tip: Personalized guidance is key — what works for one family may not work for another. We can help you find the best solution for your unique situation.

FAQ

Check Other Articles

A Million Dollar Baby

Learn how smart investing over just a few years can turn your savings into a million-dollar portfolio, with strategies to grow your wealth efficiently.

Social Security for Immigrants

Learn how Social Security works for immigrants in the U.S., including eligibility, benefits, and tips to maximize your retirement income and protect your family.

Career Opportunity

Discover how building financial literacy can open doors to better career opportunities, help manage your money wisely, and set you up for long-term success.