Why Savings Accounts and CDs May Be Quietly Costing You Money

Many people think putting money in a savings account or Certificate of Deposit (CD) is the safest way to grow wealth. And it is safe, but “safe” does not always mean effective. n fact, keeping too much money in low-yield accounts can quietly erode your purchasing power over time. Understanding the risks and exploring alternative options can help you protect and grow your money more effectively.

Here’s why your money may actually be losing value over time.

Savings accounts and CDs disadvantages

Inflation: The Silent Erosion

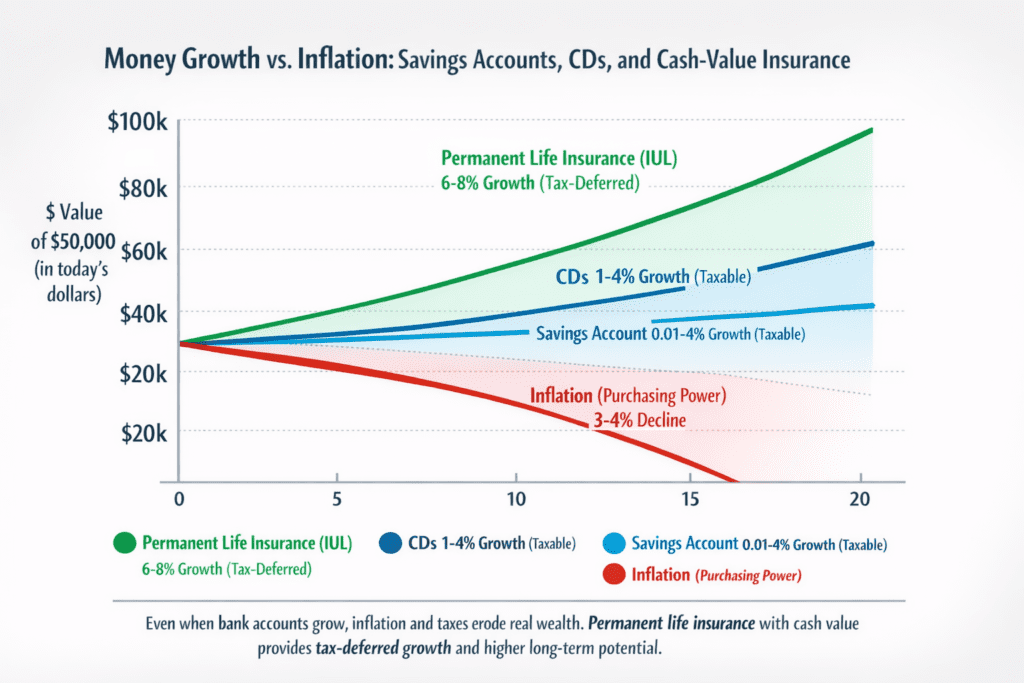

If inflation runs at 3%–4% annually, but your savings account earns only 0.01%–4%, your money might not keep pace.

The Rule of 72 helps illustrate this: 72 ÷ interest rate = years to double (or halve purchasing power)

Example:

- Inflation: 4%, 72 ÷ 4 = 18 years to lose half purchasing power

- Savings account: 3%, 72 ÷ 3 = 24 years to double nominally

Even if your account grows, you may be falling behind in real terms.

Taxes Further Reduce Returns

- Interest from savings accounts or CDs is taxable as ordinary income.

- Example: 3% interest after a 25% tax is ~2.25% net

- If inflation is 4%, your money is shrinking in real purchasing power

CDs: Slightly Higher, Still Limited

Fixed interest rates are slightly higher than those of savings accounts

Locked-in money limits flexibility

Still taxed as ordinary income

CDs protect principal but rarely outpace inflation over the long term.

Missed Opportunity: Tax-Advantaged Accounts

- Instead of letting money sit in low-yield accounts, consider:

- Traditional IRA or Roth IRA (subject to income limits)

- 401(k), 403(b), or similar employer plans

- Health Savings Accounts (HSA)

- Permanent life insurance with cash value

These options allow tax-deferred or tax-free growth and often outpace bank accounts and CDs.

Permanent Life Insurance with Cash Value

Permanent life insurance, such as whole life, universal life, or indexed universal life (IUL), offers more than just a death benefit. It can be a powerful wealth-building tool:

- Cash value growth: Accumulates tax-deferred, potentially outpacing inflation.

- Tax-free access: Policy loans or withdrawals can often be taken without taxes if managed properly.

- Flexible investment options: Indexed or variable policies can provide higher growth than traditional savings or CDs.

- Financial protection: Provides a guaranteed death benefit for your family.

- Supplemental planning tool: Can complement retirement accounts, providing liquidity, estate planning benefits, and protection against market volatility.

- Long-term wealth accumulation: Example: Contributing $20,000/year to an IUL could grow to $500,000+ cash value in 20 years, all tax-advantaged.

By combining protection and growth, cash-value life insurance can serve as both an emergency fund alternative and a long-term investment tool, making it uniquely versatile.

Savings accounts and CDs are safe, but they rarely protect your future

A smarter strategy:

- Keep an emergency fund in a safe account

- Maximize tax-advantaged growth through retirement accounts, HSAs, and cash-value insurance

- Invest in ways that outpace inflation

Even small contributions today can have a huge long-term impact.

More Articles about Financial Literacy

The Rule of 4%

Learn the Rule of 4% for retirement: how much you can safely withdraw each year to make your savings last.

Why can Social Security be so low

Understand why your Social Security payments may be lower than expected and how work history, earnings, and benefits calculations affect them.

Estate Planning

Learn how to protect your assets, provide for your loved ones, and plan your legacy with smart estate planning strategies.