Guiding Immigrants Toward Financial Security in Retirement

Planning for retirement can be challenging, especially for immigrants who may have started working in the U.S. later in life. One of the most widely used strategies for withdrawing retirement savings is the 4% rule, a simple guideline designed to help retirees access their funds without running out of money too early.

What Is the 4% Rule?

The 4% rule is a guideline for retirement withdrawals. It suggests that retirees can safely withdraw 4% of their retirement portfolio each year during retirement, adjusting annually for inflation, without depleting their savings for at least 30 years.

Why It Matters for Immigrants

Immigrants may face unique financial challenges:

Shorter U.S. work history: Social Security benefits might be lower if you didn’t work in the U.S. for 35 years.

Different retirement accounts: You may have a combination of 401(k), IRA, or personal savings.

Currency and tax considerations: Planning withdrawals in U.S. dollars and understanding taxation is critical.

Using the 4% rule can give you a starting point for planning how much you can safely withdraw each year while keeping your retirement savings intact.

Comprehensive Insights into Retirement Planning

Explore vital financial statistics that guide immigrants in applying the 4% Rule for sustainable retirement withdrawals.

4%

How to Use the 4% Rule

Calculate your portfolio

Total all retirement accounts and investments you intend to use for retirement.

Determine annual withdrawal

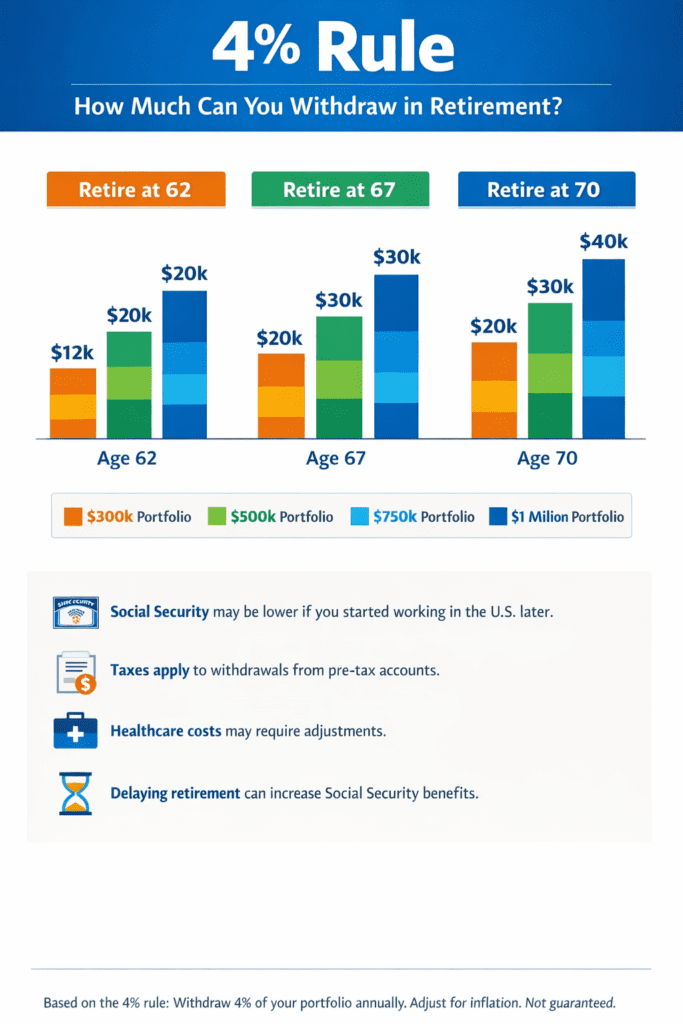

Multiply your total portfolio by 4%. For example:

- $300,000 × 4% = $12,000 per year

- $600,000 × 4% = $24,000 per year

Adjust for inflation

Increase your withdrawals each year by the inflation rate to maintain your purchasing power.

Review regularly

Market conditions, taxes, and unexpected expenses may require adjustments. The 4% rule is a guideline, not a guarantee.

65-67 retirement age

Limitations to Conside

- Market volatility: Large downturns early in retirement can reduce the sustainability of withdrawals.

- Longevity risk: If you live longer than expected, 4% may not be enough.

- Taxes: Withdrawals from pre-tax accounts (such as traditional 401(k) or IRAs) are subject to income tax.

- Healthcare costs: Unexpected medical expenses can exceed what was planned.

For immigrants, understanding tax implications is especially important if you have earnings or pensions in another country.

30

Retirement Duration

Projected years of retirement during which funds must be sustained using the 4% Rule.

20

Withdrawal Safety Margin

The buffer percentage is intended to accommodate unexpected expenses and market fluctuations.

The 4% rule provides a simple framework to help immigrants and all retirees plan for sustainable withdrawals from their retirement savings.

While it is not a guarantee, it helps you balance income needs with long-term preservation of your portfolio.

Tip: For most immigrants, Social Security alone will not be enough. Combining it with personal savings and investments, using the 4% rule, can provide a safer, more predictable retirement income.